I’ve been working in this industry for a long time – over thirty years. For most of that time, I’ve been working as a freelancer, but it’s always been working for someone else. When I set up Magnum Solutions (my freelancing company) in 1995 I always had a vague desire to grow it into a… Continue reading 2020 Vision

Category: life

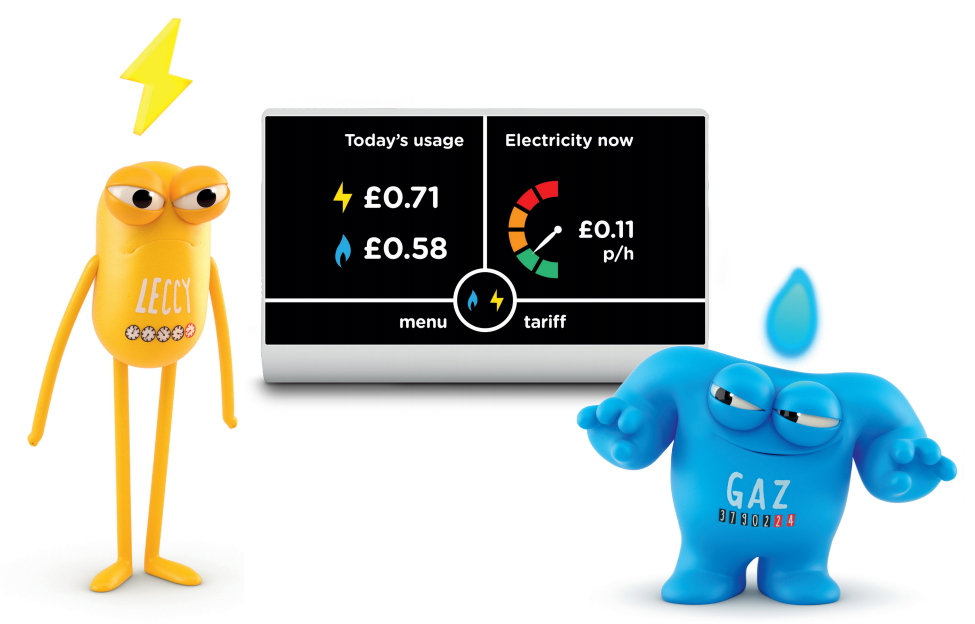

When Smart Meters Aren’t

In a process that took ten years, from 1986 to 1996, the Conservative government privatised energy supply in the UK and turned it into a competitive marketplace. The British public resigned themselves to a lifetime of scouring pricing leaflets and frequently changing energy suppliers in order to get the best deal. This became simpler with… Continue reading When Smart Meters Aren’t

Public Service Announcement: Aegon Pensions

Do you have a person pension with Aegon? If so, I suggest you ask them to double-check the statements they have been sending you, as they might well be incorrect. I’ve recently discovered that mine have been wrong to the tune of several thousand pounds for seven years. This year I’ve been transferring all of… Continue reading Public Service Announcement: Aegon Pensions

Insurance Update

Regular readers will know that two and a half weeks ago, my kitchen ceiling collapsed. A few people have asked me how things are going. Here’s an update. It’s not a happy story. I’ve been talking to Aviva to work out what needs to be done. I took out my buildings insurance through my bank,… Continue reading Insurance Update

An Interesting Evening

(But the “Chinese curse” kind of interesting) This evening I got home at my usual time, picked up my post from the doormat and was sitting on the sofa reading it. Suddenly I heard an almighty crash followed by the sound of running water. It was coming from the kitchen. I ran in and found… Continue reading An Interesting Evening

Money From HMRC

I got a letter from HMRC this morning – to my company, not to me personally. It basically said “we’ve been looking at the PAYE you paid in 2010/11 and it looks like you’ve overpaid by [a surprisingly large number of pounds]”. Now 2010/11 was the year that I was having some difficulties with my… Continue reading Money From HMRC

Ticket Refund Update

[There are two earlier posts that you might want to read before this one] I mentioned yesterday that See Tickets customer support were trying to get hold of me. I spoke to them in the early afternoon. It was their customer services manager and she wanted to apologise for the way I had been treated… Continue reading Ticket Refund Update

Five Pounds and Twenty Pence

[New readers should probably read the background before proceeding] The figure of £5.20 has come up in some of the discussion of this issue. It’s the difference between what I paid for the tickets and what See Tickets want to refund me. It’s come up in two ways. Firstly a couple of people have said… Continue reading Five Pounds and Twenty Pence

See Tickets

Anyone who buys tickets for gigs, plays or sporting events will have horror stories about how a reasonably priced ticket suddenly became a lot less reasonably priced once booking fees, transaction fees and postage fees had been added on. I’ve often wondered why the face value of tickets doesn’t just include a fixed amount that… Continue reading See Tickets

Chuggers

Earlier this week, I was stopped by a chugger in Richmond. We see a lot of chuggers in Richmond. I suppose that the charities see it as an area that still has a lot of disposable income. Usually I have my earphones in so they ignore me, but this was at lunch when I’d just… Continue reading Chuggers